Market Update – November 2021

13/12/2021

Affinity Insights – Issue 18 December 2021

17/12/2021

Around this time last year, we made three broad market predictions:

- The availability of vaccines would see a return to relative normalcy in the second half of 2021.

- A recovery in growth and higher real interest rates would drive a rotation from growth into value stocks.

- Equity markets will eventually come under pressure from rising long term interest rates.

We were broadly correct on Covid with the notable exception of China and Australia. If you are vaccinated, life is pretty close to normal in most major economies. A slow vaccine rollout and a last ditch failed elimination strategy delayed Australia’s return to normalcy. China’s persistent desire to eliminate Covid continues to impact life there in a major way.

Our performance on the other two predictions was more mixed. There was a rotation from growth to value stocks, but it was relatively short lived. Real rates remained anchored at very low levels. However, there has been recent significant weakness in the hyper speculative part of growth indexes, with non-profitable tech down around 40% from its peak. At times equity markets seemed to be stressed by rising interest rates, but rates never really rose enough to pressure markets, with the US 10-year yield peaking around 1.75% in late March. We, along with most others, underestimated the inflationary impact of Covid related supply chain disruptions crashing into a wave of demand related to economic re-opening.

Given how markets evolved this year, we were quite active in moving the portfolios around to take advantage of opportunities and avoid risks. Our expectation is that next year won’t be much different.

How might the dominoes fall in 2022?

Growth to Slow

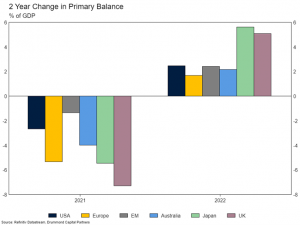

Global economic growth should slow next year. The easy gains post the removal of most Covid restrictions have occurred. Governments are transitioning from supporting economies to withdrawing stimulus (see figure below, which is a reasonable proxy). Higher inflation is eating into wages and reducing consumer purchasing power. The boost to goods consumption during Covid (upgrading the home office and online shopping with stimulus cheques) and services consumption after restrictions were relaxed (binge booking restaurants and travel) has faded. Central banks are also expected to begin winding back support next year, which will weigh on consumer and business confidence.

Inflation Moderation

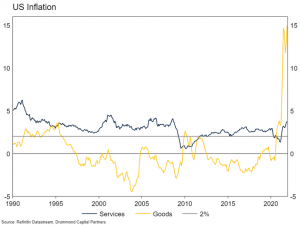

Inflation will moderate through next year but remain uncomfortably high. Some of this reflects the legacy of extreme price increases for energy and used cars which will remain in the inflation numbers due to the way it is calculated[1]. However, even after these base effects fade, inflation will be higher than in the years prior to Covid. Rapidly rising house prices and rents will boost CPI through next year, as will the impact of supply chain disruptions on goods and wages growth on services. The figure below shows this in more detail. Relative to the past decade, even abstracting from price rises in used cars and petrol, recent high inflation prints have been broad based. The Fed will look through higher energy and food prices, but if supply chains continue to pressure furniture, TV and clothes prices higher, they will be forced to respond.

Central Bank Action

As a result, major central banks will begin the process of policy normalisation next year. Although inflation and growth should slow, the former will remain too high for comfort and the latter is unlikely to fall below trend. At the moment, markets expect between two and three rate hikes next year in the USA and Australia. We think given the above, that is a little too aggressive, but not out of the question in the USA. Given high household debt levels, rate hikes in Australia will be harder to deliver. Elsewhere, policy will likely be eased in China, tightened in much of EM and flat in Europe and Japan.

The problem with this is that rate hikes are a terrible tool to fight the kind of inflation economies are facing. Higher interest costs for businesses and households in the USA do not resolve electricity shortages in China, blocked canals, or a shortage of truck drivers. Most consumer spending in rich countries is on services, which is still “under control” from an inflation perspective. Importantly, for three decades the natural order of things in these countries has been goods deflation (TVs and cars getting cheaper) and reasonably high services inflation (education, healthcare and haircuts getting more expensive). If goods inflation becomes structurally positive (due to deglobalisation, climate change adaptation or the end of China’s economic miracle) the only way to keep inflation below target will be to restrict services inflation. In practice, this means weaker growth and higher interest rates than the decade following the Financial Crisis. But we digress, this is a topic better addressed in next year’s SAA Review.

2022 US Mid-Terms

The Democrats will almost certainly lose control of Congress in the 2022 mid-terms. There are two important implications from this. In the lead up to the election, expect politicking and brinksmanship over the debt ceiling and budget process. There is not likely to be any meaningful economic reform in the year ahead. Republicans will attempt to wedge the Democrats around Biden’s proposed tax increases and Covid restrictions. More importantly, a loss of control from the Biden administration likely means a return to forced fiscal austerity – similar to the late Obama years. This will see a sharp reversal in growth expectations from the late 2020 Biden blue sweep.

More Covid Waves, But Immaterial Restrictions

Whether due to Omicron or some other new variant, a seasonal winter spike, fading vaccine immunity or simply the sheer number of people globally who have yet to be vaccinated or infected, global Covid cases will probably drive the news flow again at some point next year. Assuming the next wave is driven by the Omicron variant (which seems the most likely culprit at this stage), it will be accompanied by significant (and politically scary) case numbers. Given early evidence suggests that prior infection and vaccination provides reasonable protection against severe illness, we do not expect governments to enact renewed punitive Covid restrictions en masse. However, various combinations of vaccine mandates, mask wearing, lockdowns for the unvaccinated and capacity limits will be implemented (or maintained) in many jurisdictions. The market impact from the above will be limited.

The wildcard here is China, which is still pursuing a zero-Covid policy by implementing strict lockdowns and quarantine following every outbreak. In a world already suffering from significant supply chain disruptions, ongoing lockdowns within China will continue to drive goods shortages and contribute to ongoing inflation volatility.

China Lightens Its Regulatory Touch

In large part, China’s economic growth next year will hang on whether the Government decides to reflate the economy again via housing and infrastructure spending or whether they accept a period of lower growth to help de-risk the economy. The recently concluded Central Economic Work Conference refocussed attention on growth, noting “the triple pressures of demand contraction, supply turbulence and weakening expectations” and seeing the external environment as “more complex, severe and uncertain”. Highlighting the importance of the 20th Party Congress next year, the meeting called for stability and vowed to “keep the economy operating within a reasonable range”.

Stability isn’t necessarily reflation, but it seems increasingly likely that more policy easing will be required to maintain an acceptable rate of growth in the years ahead, particularly if the transition towards a more state-orientated property development sector continues to proceed, flushing out the more speculative operators, but reducing overall construction activity.

Asset Class Implications

So, what does the above outlook mean for expected asset class returns? Below, we use our capital market framework to quantify this 2022 outlook. Clearly, 1 year asset return forecasts are fraught with danger, but they are broadly indicative of what we think is achievable in this environment, likely with considerable volatility through the year.

Cash, Bonds and Credit

The return to global cash will improve a little next year as central banks begin the rate hiking process. However, we think there is little chance that the RBA will keep up the pace. As a result, returns to cash are expected to remain low.

Long term bond yields are probably a little too low at present, but we don’t believe that developed economies are strong enough to stomach the sort of rate rises currently priced into markets. As a result, we think prospects for 10-year yields being sustained above 2.5% in the USA for any length of time in 2022 are low. Regardless, even this small increase in yield implies capital losses and a negative return to the asset class in the year ahead. Australian bonds fare better as we do not believe the RBA will be as aggressive as other central banks in its hiking cycle.

We also expect mildly negative returns for credit, accounting for some spread widening and expected default rates. Investment grade credit will also be weighed down by rising interest rates.

Equities

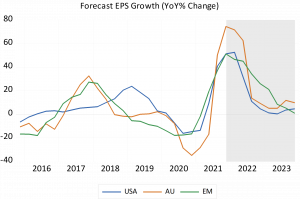

The easy gains for equities have been made and we expect 2022 to see multiple compression for the US market in particular. Earnings growth is also expected to slow significantly (see below). In line with this, we see modest, but positive equity market returns next year. Within equities, we see the Australian, UK and Japanese markets as the strongest performers, reflecting a combination of more robust earnings growth and less valuation pressure.

Taking a more holistic view, this forecast understates the ride we expect from equities next year. Though positive returns are the most likely outcome, we expect substantial volatility as markets digest the mix of high (but moderating) inflation, tighter central bank policy and slowing economic growth. We think equity markets will “feel” largely rangebound, driven by reasonable dips and rallies through the year. We expect ample tactical opportunity around key policy events in particular.

Alternatives

We expect modest returns to alternatives including hedge funds and real assets next year. Hedge funds struggle in low cash rate environments and tend to do poorly when picking turns in macro policy as they are often heavily influenced by systematic factors. REITs will continue to struggle to deliver earnings in an environment of ongoing reduced office demand and Amazonification of retail centres. There will however, be pockets of performance to be found in assets which take advantage of these thematic changes. We think infrastructure will be in large part influenced by ongoing travel restrictions due to Covid and the ongoing push to choke capital financing from carbon intensive businesses.

Portfolio Positioning

We will more than likely (unless there are significant changes in the next few weeks) enter 2022 with a relatively neutral position outside of a reasonable bond underweight. From a portfolio positioning perspective, if we are correct in the above, we will likely add to equity exposure on corrections and move back towards neutral when previous highs are met. If long term bond yields manage to achieve a 2% level, we will build a more substantial position unless it looks as though inflation is not moderating (in which case we will likely reduce equity exposure as well). A more attractive bond return reduces the need for alternatives in the portfolio which will be the likely funding source. We are likely to be quite tactical around emerging market equities next year, as much hangs on the directives of the Chinese government, which is incredibly difficult to predict ahead of time.

In a slowing growth environment, we will be hesitant to hold much value exposure within equities. That said, rising interest rates don’t bode well for growth stocks either. As such, we will likely maintain a focus on quality, as has been our objective for much of this year. With the A$ around the bottom of its recent trading range, we prefer hedged equity managers. This is likely to reverse if the A$ moves back towards the middle of its 70c – 80c fair value range. Within credit, we expect a continued preference for floating rate and loans, which will avoid capital losses from rises in long term interest rates.

[1] Statisticians call this the impact of base effects. Monthly data prints remain present in an annual percentage calculation for a year.

This Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, a Corporate Authorised Representative of BK Consulting (Aust) Pty Ltd (AFSL 334906). It is exclusively for use for Drummong clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

.