Four personal finance books to give your children… and the lessons they will learn

06/06/2022

5 Cognitive biases that will stop your children making smart financial decisions

28/07/2022

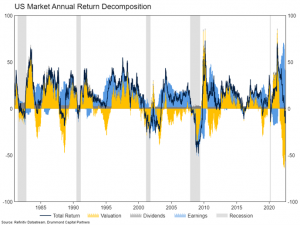

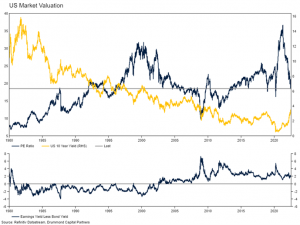

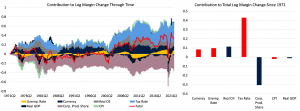

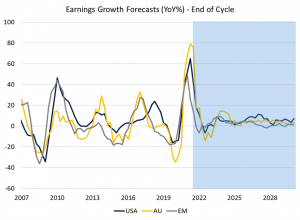

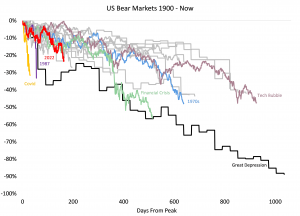

Key Points: The US equity market has now entered its third bear market (greater than 20% market sell-off) in under four years – the quickest hat trick in at least 120 years. Global equity markets have been under pressure all year, largely due to persistent inflation and the resultant tightening in monetary policy from central banks globally. Equity markets have faced a valuation hit from higher discount rates as long-term interest rates have risen and have begun to price in the risk that tighter monetary policy will eventually lead to a recession. In this month’s Market Update, we take a deep dive into equity bear markets and their drivers. A History of Bear Markets There have been 21 US bear markets since 1900 – one every five to six years on average. The average total sell-off is around 35% over a period of around one and a quarter years. There have only been three US market falls greater than 40% since the 1950s – the 1970s recession, the Tech Bubble, and the Financial Crisis. There were many large sell offs between 1900 and the Great Depression, but comparisons this far back in time are not as useful as those with more modern episodes. In 1915, there were only twelve companies in the Dow Jones Index, economic policy making was vastly different and market structure was archaic relative to today. Relative to previous bear markets, there is not really anything particularly special about the current episode (see below, in red). The pace is a little faster than average, though the 2018, Covid, Great Depression and Black Monday drawdowns were all significantly faster. With the market down just over 20%, the sell-off to date is less than the average – but of course it may not be over (more on this below). Market Return Drivers If the current correction is relatively “normal” in aggregate, what about the underlying drivers? Below, we break down equity market returns into dividends, earnings growth, and valuations. In periods of substantial equity market weakness, it is common for valuations to compress (yellow slice falls) while earnings remain healthy. Then, a good way after this point, and often after equity markets have begun their recovery, earnings (the blue slice) fall. However, if equities are recovering, this is more than made up for by an increase in valuations. Large and protracted drawdowns and recessions, such as the Financial Crisis, face declining earnings and valuations. Dividends (grey slice) tend to be quite stable through time. While they are a significant contributor to long term returns, on a year-to-year basis they have limited impact. We can see from the chart below that the first half of that pattern has taken place. Of particular interest is the magnitude of the compression in valuations. The current profile is the largest in fifty years. While the US equity market has sold off, it has been in large part insulated from this by very impressive earnings growth. This earnings growth (and the market fall) has taken the trailing PE of the US market from a peak of around 35 times earnings in April 2021 to around 21 times today. This has kept the valuation spread between the equity market and the bond market (lower pane in chart below) relatively flat, despite the largest increase in bond yields in many decades. It is possible to make the case using the chart below that the current drawdown is entirely reflective of valuation adjustment driven by higher bond yields. Relative to bonds, US equity valuations are basically flat. Do Markets Keep Falling? With markets already off more than 20% and valuations having improved significantly in absolute terms, what is next? Mechanically, any further correction must come in the form of lower valuations, dilution (share issuance) or lower earnings. A correction in valuations could come from higher interest rates or increased concern about the risk of a recession. As we have mentioned in previous notes, we think the increase in long term interest rates (cash rates will continue to increase) has largely run its course. Ongoing multiple compression driven by fears of recession is certainly possible, but the fall that has already taken place is pretty extreme. The trailing PE ratio for US equities has fallen around 40%, the same magnitude as in the Tech Bubble and Financial Crisis. The only larger fall was in the 1970s correction of 62%. Given inflation has been key in both episodes, our expectation going forward is not for a decade of extremely high inflation, so this comparison is perhaps not the most valid comparator. In absolute terms, the trailing PE ratio remains elevated compared to the immediate post Financial Crisis period but is not that much higher than during the depths of Covid and is lower than the entirety of the Tech Bubble. As an aside, major markets outside the USA are also pretty cheap. Dilution is common in periods of economic and financial market stress, particularly when companies cannot access debt funding markets, or the cost of that debt is prohibitively high. In the short term at least, this does not seem particularly likely. Earnings remain healthy and wholesale equity issuance is more of a last resort tool for corporates. That leaves earnings. Earnings growth is largely a function of economic growth and profit margins. Profit margins for US listed corporates are incredibly high at the moment, causing some concern that a normalisation could see earnings fall sharply. However, our analysis suggests that the general increase in margins over the past 50 years reflects falling corporate tax rates (see right hand chart below). Partly offsetting this has been the share of productivity growth which has flown to workers rather than corporations between 1970 and 1980 – though this has stayed largely flat since then, supporting profit margins. Other variables such as economic growth, the unemployment rate and inflation are more cyclical. Given this, we would expect if economic growth were to slow into a recession, margins would fall, reducing profits. Source: Refinitiv DataStream, Drummond Capital Partners. Red = negative coefficient in RHS chart Another way to assess the outlook for earnings growth is using our capital market framework. Below, we show the output of our earnings growth models for the End of Cycle Scenario. In this scenario, we model a relatively small fall in earnings across major markets. This reflects as assumption of an only minor recession, similar in magnitude to the 1990s. At a high level, this scenario assumes an only minor economic contraction because corporate and household balance sheets in the US are very healthy (household debt to GDP in the US is around 2003 levels and corporate debt to GDP is around the post 1990s average), and there are no obvious excesses or imbalances in the financial system (outside of crypto, which is irrelevant from a system wide perspective). We also assume in this scenario that interest rate increases broadly consistent with current market pricing and the small recession are sufficient to get inflation back under control. Source: Refinitiv DataStream, Drummond Capital Partners Summing Up Over the medium term, earnings will be key to the next leg of equity market drawdown. While not a guaranteed outcome, a recession in the next year is more probable than not in our estimation. A forecast for slowing growth is also supported by our growth barometers, all of which are now in negative territory (see below for the US). This recession would deliver the contraction in earnings required to bring the current bear market into the territory of the average market drawdown, around 35%, or 10% to 15% lower than now. Source: Refinitiv DataStream, Drummond Capital Partners Portfolio Positioning In line with this outlook, our portfolios are currently underweight growth assets, very underweight global equities, and long government bonds. The risk to this positioning would be a significant bear market rally, which is certainly possible given the profile of market drawdowns shown in the first chart in this Market Update. Markets tend to not go down in a straight line. Otherwise, if global central banks manage to get inflation under control while avoiding a recession in the second half of this year, the current starting point for market valuations, combined with a policy easing, would present an attractive entry point for equity market investors. Any relaxation in central bank policy would likely be a catalyst for a material market rally. This is prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, a Corporate Authorised Representative of BK Consulting (Aust) Pty Ltd (AFSL 334906). It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice. .The Bear Growls

Source: Refinitiv DataStream, Drummond Capital Partners. 1900 – 1950 data is monthly Dow Jones Industrial Average. 1950 – 1963 is daily Dow Jones Industrial Average. Post 1963 is the S&P500 Index.