Reading the Crystal Ball for 2021

24/11/2020

Affinity Insights – Issue 14 December 2020

17/12/2020

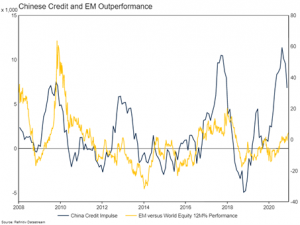

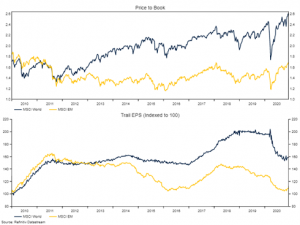

Emerging market (EM) equities have been the best performing growth asset class in the past six months, beating the developed market (DM) index by around 10%. Is this the beginning of a reversal of EM fortunes after a decade of disappointment? In this note, we investigate the reason for the recent outperformance and outline why we think a meaningful exposure to EM over the long term makes sense for portfolios. Around 5% of the outperformance is directly related to the weakening US$. However, there were more fundamental factors at play as well. China, Hong Kong, Taiwan and South Korea, countries with a substantial weight in the EM index, did not suffer a significant Autumn Covid wave (unlike the US and Europe) supporting their economies. The acceleration in credit growth in China also supported EM equities. There is a strong correlation between the relative performance of EM and DM equities and the Chinese credit cycle (see below). EM equities have also benefited from having less growth/technology exposure than the DM index, which was hurt by the growth/value rotation in November. Of the above list, the only feature which is potentially enduring is the growth/value rotation, a topic we have written about frequently this year. After falling around 10% in 2020, the US$ is now very close to its long run average value. A meaningful rebound in global growth will be needed to shift the currency significantly lower. EM Covid related outperformance will disappear next year with the vaccine roll out. Indeed, it may even go the other way given lack of vaccine supply in EM relative to DM. Chinese credit growth has also peaked. Long term interest rates and credit spreads have risen, increasing the cost of debt for Chinese corporates. The Government also allowed a few significant State-Owned Enterprises to default on their debt in recent months, which will tighten financing conditions further. Now that the short-term outlook looks less attractive given positive catalysts for outperformance are fading, we also need to consider the fact that EM performance over the past decade has been underwhelming. A lack of US$ earnings growth over the period (despite strong domestic economic growth) has played a large part. The broad MSCI EM FX basket fell by around 30% between mid-2011 and early 2020. While there are certainly exceptions, from the general perspective of a foreign investor in EM businesses, a weaker currency is not desirable. Following this decade of poor earnings growth, EM equities are trading at lower price to book multiple than in the beginning of 2010. The price to book multiple for DM equities has risen around 50% over the period. However, the combination of reasonable valuations and cheap currencies leaves EM equities with a good starting point for returns in the coming decade. EM currencies should be supported in the decade ahead by capital inflows. Emerging markets are the only countries which now offer investors positive real interest rates. While EM interest rates have fallen alongside those in DM, there is still a meaningful spread of around 3½ percentage points on offer from an absolute perspective in these countries in aggregate. In a low yield world, this will encourage inflows. In addition, as China continues on its path to becoming the world’s largest economy, many investors will see an allocation to the Renminbi as a necessary portfolio diversification decision (alongside existing allocations to Euro, Pound and Yen). We expect economic growth to continue to be stronger in EM than DM in the decade ahead. This is not a controversial forecast and simply reflects higher labour force growth (growing the pool of potential workers) and higher productivity growth (there is more capacity for productivity growth in EM due to catch up effects and lower hanging fruit when it comes to economic reforms). With stable to rising currencies, corporates in emerging markets will be able to convert this top line revenue growth into hard currency earnings in the decade ahead, boding well for future returns. The net of the above means that, based on our capital market forecasts, EM equities offer a substantial return premium to global and Australian equities in the decade ahead in our “baseline” return scenario. Coming as no surprise to anyone, this higher expected return comes with elevated risks. The information contained in this Market Update is current as at 17/12/2020 and is prepared by Drummond Capital Partners ABN 15 622 660 182, a Corporate Authorised Representative of BK Consulting (Aust) Pty Ltd (AFSL 334906). It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.Emerging Markets