Market Update – December 2023

19/12/2023Protected: Market Update March 2024

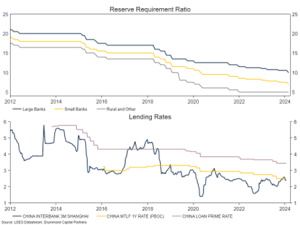

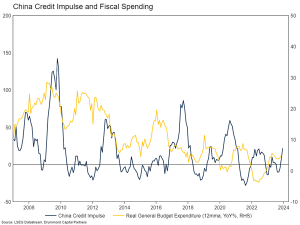

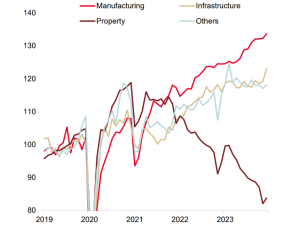

19/03/2024Key Points: In the middle of 2023, we wrote Waiting for Stimulus – a Market Update highlighting that China’s economic and market doldrums would likely continue until sufficient stimulus was put in place to restore confidence in the economy, particularly the property market. Since then, the doldrums have indeed continued. While there has been some fiscal stimulus, the equity market continues to underperform, the property market continues to contract, and overall growth remains lacklustre. In this month’s Market Update, we look at what 2024 holds. Will the fiscal stimulus gain traction? Will deeply discounted Chinese equities attract buyers? Will the property market find a floor? It is Drizzling Stimulus China does stimulus differently to major developed economies. As a government-directed economy, there is substantially more tinkering around the edges than we see in Australia. The Government will set different lending rates for different sectors, direct the investments of state-owned enterprises, favour certain industries over others. While more control is great when it works, it can have unintended consequences which are hard to account for in something as complicated as an economy. In China, the largest of these unintended consequences has been too much debt accumulated by local governments for unproductive investment, and a (probably) oversupplied housing market whose prices make Sydney look reasonable. When your largest problems are the result of previous stimulus efforts, how do you stimulate your way out of them? The answer to this question is: carefully. This has been China’s approach for the last six months. In January 2024, the Government cut reserve requirement ratios, which frees up around RMB1tn (~$215B AUD), or ~1% of GDP, in bank lending liquidity. They also cut lending rates for small/medium businesses and agriculture producers. In late 2023, they cut primary lending rates a little. Most expect they will cut a little bit more in the first half of this year. Late last year, the Government also announced a further RMB1tn Central Government bond issuance, which should support economic growth this year. There has also been substantial tinkering, with lots of policy announcements providing support for property developers and the housing market. Overall, this easing has seen China’s credit impulse pick up, and fiscal spending increase. However, the magnitude of the rise in both has been limited relative to previous easing cycles. A Little Recovery While muted, the stimulus and easing to date looks to be putting a floor under overall economic activity in China. Our growth barometer shows a generally improving trend since the middle of 2023, though so far to only a very modest level of activity. Economic growth in China in 2023 was just above 5%, weak by historic standards and disappointing considering 2023 was a post Covid-lockdown recovery year. However, it was just above the Government’s growth target, perhaps giving them confidence that the easing to date has been sufficient. Source: LSEG Refinitiv, Drummond Capital Partners However, sufficient economic growth does not necessarily translate into equity market outperformance. Since growth began to improve in the second half of 2023, China’s equity market has continued to underperform pretty much everything else. In response, the regulator has restricted short-selling, tightened capital controls, and prevented some investors from being net-sellers of equities. More recently, there have been rumours of a RMB2trn stabilisation fund, which could utilise funds in the offshore accounts of Chinese SOEs to purchase onshore stocks. Similar market friendly policy efforts were put into place in 2015, though at that time the equity market did not find a floor until it was clear property sector weakness was resolved. Where to From Here? The economic recovery in China is not being helped by the property market. The figure below shows fixed asset investment by sector. Manufacturing and infrastructure capex are driving the overall outcome while property investment continues to fall. Weak property market outcomes are also hurting the services side of the economy. Retail spending on construction and decoration material, furniture and electric appliances is around 30% below its long-term trend. Source: NBS, CEIC, Société Générale Cross Asset Research / Economics Fixed Asset Investment (Index, SA) High frequency housing market data shows no recovery in transactions so far and house prices continue to fall. Prices may yet have a good way further to go. Affordability is a challenge. The national average house price sitting at 12 times income and Tier-1 cities are multiplies of that. In NSW, the mean dwelling (including units) price is around nine times household income. At the same time, China is probably building too many dwellings (while Australia is not building enough). Since 2000, dwelling investment in China has risen around 50-fold, compared to three-fold in Australia – and Australia has had much stronger population growth. With too many, too expensive, dwellings, it is hard to see what turns the property market in China around outside of more meaningful government support. Ironically, meaningful government support for the sector is the source of the problem in the first place. In our estimation, the most likely outcome is continued piecemeal support, aimed at stabilising the economy and avoiding an outright crash. Market positive measures could involve more reserve requirement ratio and interest rate cuts and another lift in the Government bond issuance target. These are both expected by the market for this year, though as with 2023, probably to a lesser extent than other policy easing cycles. Less important for the market, but still necessary to stop the rot, would be lessening restrictions on multiple property purchases and programs to restructure the bad debts of property developers and local government financing vehicles. Another key question is how much more damage to the equity market can actually be done? The index of Hong Kong listed property developers has fallen around 60% from the peak. That is less than the index fell in the Financial Crisis, and a good way from the 85% US homebuilders fell over that period. There is historic precedent for larger falls. Portfolio Positioning The overall China onshore market is obviously further from the fire than homebuilders, and it is still around 40% from its peak, a good-sized correction. China A is trading at a price to book ratio of 1.4 times, compared with 2.2 times for global equities as a whole. If the market keeps falling, will global investors begin to see value? We think while the overall market might find a floor alongside the economy this year, we will need to see a proper resolution to the housing market crisis before the path is clear for excess returns. We have no structural allocation to emerging markets. Rather we allocate tactically when we think they can outperform developed markets. If the resolution to the Chinese property crisis comes in the form of a multi-year period of sluggish growth and economic restricting, we may be out of the Chinese market for a good while. That said, sideways is a difficult path to navigate for policymakers, particularly for those struggling to balance a slowing economy with building systemic risks. With a shrinking population and deflation seeming to be taking hold in China, policymakers may be glancing across the East China Sea and worrying about replicating Japan’s multi-decade economic stagnation. A temporary fix to these concerns could be a large-scale stimulus of the kind seen following the 2015 slowdown. If this is the case, we think a temporary allocation to the region could be fruitful. For now, we remain in wait and see mode. This is prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice. .Uncertainty in China Continues