How to make sure your children are ready to eventually take over your wealth

01/12/2022

Affinity Insights – Issue 20, December 2022

23/12/2022

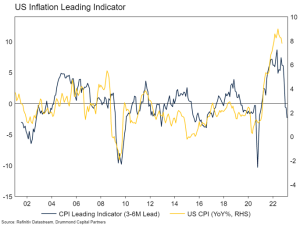

Key Points: This time last year[1], we made some broad predictions about what we thought 2022 would hold. We got the outlook mostly right. In the “win” column, we correctly predicted growth would slow, reflecting the withdrawal of Covid fiscal stimulus and tighter monetary policy. We thought the world would walk away from Covid restrictions, despite high case numbers and we expected China to ease off on regulatory tightening. In the “tie” column, we thought inflation would moderate through the year. The jury is still out on that prediction, though it does appear as though inflation has peaked. We also thought central banks would tighten monetary policy, but we (and everyone else) materially underestimated the extent of monetary tightening that has taken place so far. We did not foresee Russia’s invasion of Ukraine. In terms of asset class return predictions, our performance was reasonable. We expected negative bond and credit returns, which has been the case. We thought equity returns would be volatile, but slightly positive. However, global equity markets are negative year to date. We also expected Australian equities to outperform global and emerging market equities, which has been the case so far this year. Inflation and Growth Regular readers of our Market Updates will know we expect 2023 to feature a recession across major developed economies. There are a number of reasons we hold this view. We also expect inflation to fall over the year ahead, which complicates the picture for markets. The forecast moderation in inflation reflects falling goods prices as Covid related supply shortages are eased and retailers find themselves overstocked in the face of weaker consumer spending. Housing related inflation should ease as house prices fall and the unemployment rate rises. The services side of inflation will be stickier, reliant on a rise in the unemployment rate and lower wages growth to ease pressure. Nevertheless, the net of the mix should see lower inflation. How markets digest this will depend on the extent of economic and earnings growth weakness. As long as inflation moderates but growth remains robust (either because we are wrong about a recession or it takes longer for the downturn to eventuate), equity markets should respond positively (as they have done so far this quarter). However, we do not think we are too far away from the point at which economic weakness becomes more evident in data. Our Growth Barometer has been generally negative since April this year. Indeed, it is showing a slowdown in activity of greater magnitude than seen during the European Sovereign Debt Crisis or the 2018 trade war and Fed policy tightening episodes. Many global PMIs as well as the US ISM are indicating shrinking global manufacturing output. In line with this, we expect the market’s attention will soon turn towards how high the unemployment rate could rise and how far corporate earnings estimates should be cut as expectations for a recession build. Source: Drummond Capital Partners Most commentators expecting a recession next year are forecasting it to be quite modest. Expectations are for only a small increase in the unemployment rate, around one or two percentage points versus an increase of more than five percentage points in the Financial Crisis. We agree there is a higher-than-normal chance that an eventual recession will not be too painful. There are no obvious major systemic imbalances (such as the global banking system in the Financial Crisis) and households and corporates in most large, developed countries enjoy healthy balance sheets (with some exceptions). In addition, the downturn is almost entirely driven by policy makers, suggesting that if growth falters too much, subsequent rate cuts could go a long way to kickstarting economic growth once more. More Rate Hikes? The market is pricing a little more policy tightening by central banks in the first half of 2023, then either unchanged rates or minor cuts in the second half of the year. This is broadly consistent with our expectations, though with some nuance. For the Fed, assuming rates rise to around 5%, this would be the largest tightening cycle since the 1980s. Prior to the Financial Crisis, the Fed took rates from 1% to 5.25% between mid-2004 and mid-2006. This time around, the market is pricing the Fed to do a little bit more (starting from 0%-0.25% rates) in half the time. Source: Refinitiv, Drummond Capital Partners Generally, the market’s relative expectation for policy tightening across countries reflects their sensitivity to debt (proxied in the chart above by household debt to GDP). Countries with very high debt levels, such as Canada and Australia, have lower expected terminal interest rates. Europe and Japan are exceptions to this, where moribund potential economic growth means even minor tightening has a very large impact. There is some risk that the Fed in the US will have to take rates higher than markets expect as households’ sensitivity to interest rates is lower than other major economies given the prevalence of long-term fixed rate mortgages. Overall, these market expectations seem reasonable to us, the key point being that the bulk of the work in terms of lifting interest rates will have been done this year. We think large scale rate cuts next year are unlikely. Though trending down, inflation is still likely to be elevated and central banks will want to be sure they have tamed the inflation beast before again easing policy. China Changes Policy Tack A change in policy regime in China has already begun and we think the process will continue into next year. These changes relate specifically to the housing market and Covid. With respect to the former, many of the policies which were put in place in recent years to stem excessive lending and risk have been wound back or paused. Turning off the leverage taps to property developers evidently caused too much damage for policy makers to stomach given the huge importance of the sector to the overall economy. The Government has tried to offset the drag from housing using broad policy easing tools, but they have so far been unable to engineer a recovery in growth. This may have something to do with the second element of policy change – walking back Dynamic Zero Covid. Prior to the 20th National Party Congress in October this year, China was unrelenting in its approach to quelling any Covid outbreak via harsh lockdowns and Orwellian population surveillance. Since then, there have been a number of steps taken to walk back that approach. The Central Government outlined 20 Optimisation Measures which cut quarantine requirements and contact tracing among many other things. The Government has also placed some of the blame for harsh lockdowns on local Governments. In response, cities and provinces have also reduced restrictions, ambitious targets have been set for vaccinating the elderly and Government propaganda publications have been producing content downplaying the severity of the Omicron variant. With cases still rising sharply, we expect the winding back of Covid restrictions to continue early in the new year, paving the way for a full reopening. While this will potentially allow stimulus measures to support growth through the year, we think the market is understating the overarching weakness in the housing market, which will prevent an economic recovery of the nature seen in previous stimulus cycles. Grey Swans The above outlook is relatively close to current market consensus, though we would argue that consensus moved towards our longer held view rather than the other way around. Importantly, there are a number of ways the global economy could pivot, spoiling the outlook. Expected Returns Acknowledging that one year forecast asset class returns are fraught with danger and will almost certainly be incorrect, we still think it is instructive to demonstrate how our forward view of the investment environment may translate into asset class returns if we are entirely correct. Overall, we expect reasonable returns to cash and bonds, reflecting this year’s rise in interest rates. For longer dated bonds, downward pressure on yields from lower growth and inflation expectations should be broadly offset by still high shorter term interest rates, meaning we do not expect a wholesale change in capital values until central banks start cutting cash rates. However, the increase in yields means the carry earnt from bonds is much better than has been the case over the past decade. Credit and equity returns are expected to be negative, reflecting a forthcoming recession. Australian equities are expected to outperform global equities reflecting their more defensive characteristics. Our previous analysis[2] suggests that equity markets do not bottom during a recession until inflation has peaked and central banks are well into a policy easing cycle. In a normal environment, the lags between monetary tightening and economic growth suggest this year’s rate hikes will begin to be meaningfully felt from the middle of next year. This suggests a recession begins middle to late 2023 with interest rates to be cut late 2023 or early 2024. There are some caveats to the above. Europe is likely already in recession given the energy price shock. Australia may enter a recession later given the RBA has lagged other central banks in hiking rates (and may even get lucky again and avoid one if history is any guide). Strong consumer balance sheets in the US may see households hold out a little longer than normal before capitulating and reducing spending, which may delay a recession there until early 2024. Rate cuts may be delayed if inflation does not fall as much as hoped. All of the above suggests to us the equity markets will not find a bottom in the first half of next year and moderately low forecast expected returns for 2023 likely feature a first half downturn and some recovery late in the year. Returns to alternatives should be generally insulated from this pain (given their generally market neutral nature). REITs and infrastructure relative returns are influenced by relative starting valuations. Infrastructure has outperformed over the year, but the underlying companies are still sensitive to economic activity and falling commodity prices. REITs have been badly punished following Covid drawdowns and then higher interest rates, with the impact of the latter arguably already having washed through the asset class. Source: Drummond Capital Partners Portfolio Positioning Current portfolio positioning is broadly in line with the expected returns above. The portfolios are underweight equities and credit and overweight cash and alternatives. This positioning is likely to be relatively stable (notwithstanding attempts to trade the bear market rallies and drawdowns over the next year) until a recession is evident and central banks cut rates, or it is clear that inflation is moderating of its own accord and a recession is not necessary to reset inflation lower. In either case a higher allocation to growth assets would be warranted. [1] https://www.drummondcp.com/insights/looking-to-2022 [2] https://www.drummondcp.com/insights/are-we-there-yet This is prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice. .Reading the 2023 Tea Leaves