Proposed tax concession changes and what it means

02/03/2023

Rise of the Machines

03/04/2023

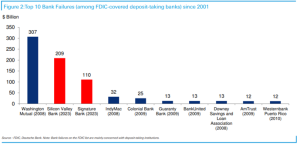

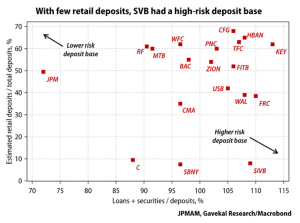

Key Points: Though last week’s US bank failures were relatively small in the context of the total US banking system, they were large in the context of historical bank failures. Authorities were rightly concerned that the failures would spark wider bank runs, which would likely lead to a larger financial crisis. Although, bank deposits are guaranteed up to US$250,000 and the vast majority of accounts in regular banks are well below this limit; bank runs are driven by sentiment rather than logic. Importantly, this program ensures depositors are made whole, but holders of bank debt and equity will see losses. It is also important to note that SIVB and SBNY aren’t exactly pillars of risk management. The chart below shows they had a generally higher risk deposit base than their peers. SIVB managed its balance sheet poorly and conducted its business in a borderline unethical way. SIVB offered discounted mortgage rates to start-up founders who deposited their VC funding at the bank – funding which could have earnt a higher yield in the US money market and should have been managed by a corporate treasury. The most important consideration from here is whether the measures put in place will be sufficient to prevent further contagion. Although, the FDIC technically only guaranteed uninsured depositors at SIVB and SBNY (to backstop the whole system would require an act of Congress), there is now a reasonable expectation that failures of other important banks will enjoy similar treatment. The new funding facility from the Fed will support bank liquidity. It is too soon to tell if more banks will face a run and consequently fail. Even if your deposit is guaranteed, as a depositor going through a bank failure is worrying and reimbursement isn’t instantaneous. Business account holders should be especially concerned given the importance of working capital and meeting payroll. It is easy to imagine a scenario where small and regional banks bleed deposits to larger institutions and need to be wound up through time as they become unviable. We would expect the regulatory burden on the overall banking system to increase given the implicit total deposit guarantee, which will be a burden for the smaller banks. However, people are often unmotivated with respect to personal finance and changing banks is a hassle. If there are no more failures this week, perhaps apathy will kick in and the status quo is maintained. The biggest implication for markets (assuming no large banking crisis is around the corner) is the change in market pricing for interest rates in the US. Markets were pricing more rate hikes this year in response to sticky inflation, a tight labour market and robust growth. Now, markets are pricing around three rate cuts by the end of the year. If last weekend’s package was sufficient to prevent a wider crisis, we don’t think the Fed will be cutting as two small banks failing in the US doesn’t really solve the inflation problem. This is prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice. .Crisis Averted?