Affinity Insights – Issue 22, July 2023

01/07/2023

Market Update – October 2023

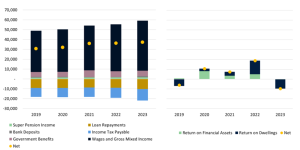

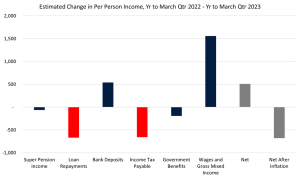

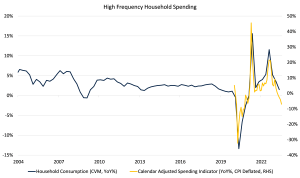

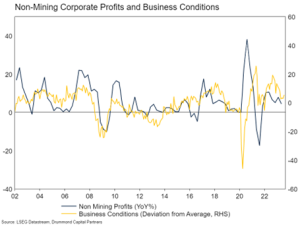

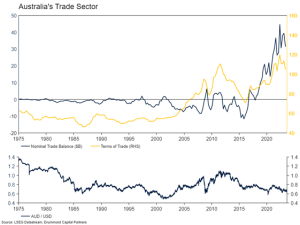

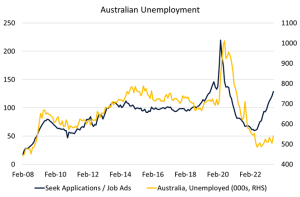

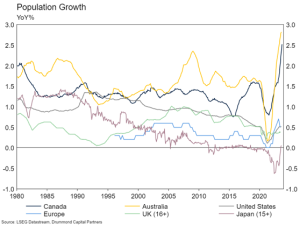

24/10/2023Key Points: In this month’s Market Update, we look under the hood of the Australian economy to see the winners and losers from what has been the fastest rate hiking cycle since the late 1980s. Households Households in Australia say they are unhappy. Consumer sentiment is lower than it was during Covid lockdowns or the Financial Crisis. Yet, restaurants seem busy, our highways are packed with Land Cruisers towing caravans and domestic air travel has recovered to pre-Covid levels. The unemployment rate is near a multi-generational low and house prices are again rising. Clearly high interest rates and inflation are having an impact on how people feel, but what about their actual financial situation? Below, we dive into the average Australian’s household accounts to see if there is a disconnect between sentiment and reality. The charts below show an estimate of per person cash flows and changes in asset prices since 2019. In aggregate, net cash flows have not grown a whole lot since early 2021 (left chart), but the outcome has not been calamitous either. On the asset side, 2023 was not a great year for households, with falling house prices dragging around $10,000 per person from household wealth. However, this comes after three years of very strong gains in wealth and in practice, household spending has a pretty loose relationship with asset price returns anyway. Source: Drummond Capital Partners, Refinitiv Datastream, ABS. Year to March quarter. Selected items. The below shows the inward and outward cash flows since the RBA started hiking rates. Loan repayments in Australia have risen by around $750 per person per year, but this has been mostly offset by higher earnings on bank deposits. This will change as more households roll on to variable rate mortgages in the period ahead and if households run down savings to fund spending. The biggest increase in cash flow has come in the form of higher wages and small business income. While some of this has been lost in the form of higher income tax (as is to be expected) the net effect has been quite strong. Importantly, there has been a big difference between nominal and real (after inflation) net cash flows. While nominal net cash flows have risen over the period, in real terms, net cash flow per person is down nearly around $750 per year. Source: Drummond Capital Partners, Refinitiv Datastream, ABS The strangest result in the above is the change in net cash flows associated with loan repayments and bank deposits. Conventional wisdom would suggest that higher interest rates would be a larger net drag. However, we can see from the charts below that the impact this time has been more muted. The chart shows three broad phases of household interest rate sensitivity. In the early 1990s, large changes in interest rates had muted impact on net cash flows (green), probably due to subdued debt levels. In the 2000s, net cash flows were highly sensitive to interest rates, given higher debt loads (red). Now, it appears as though a high proportion of fixed rate borrowing, and high levels of household deposits have muted and delayed the impact of this tightening cycle, despite record high consumer debt levels (blue). Source: Drummond Capital Partners, Refinitiv Datastream, ABS Notwithstanding the above, the drag on real household cash flows is not surprisingly beginning to have an impact on real household spending (see chart below). Indeed, based on this and terrible consumer sentiment we would not be surprised to see spending deteriorate further the quarters ahead. Especially given the data in the charts above reflects the March quarter of this year and many more households have shifted to a higher variable mortgage rate in the intervening period. Source: Drummond Capital Partners, Refinitiv Datastream, ABS Businesses Unlike households, Australian businesses seem to be feeling OK. Business confidence is around the long-run average, and non-mining corporate profits have been growing robustly. Mining profits have fallen reflecting lower commodity prices but are still elevated relative to history. In addition, capital expenditure in the non-mining sector has been rising and plans for future capital expenditure are also quite positive. Business credit growth remains solid, though has moderated somewhat from what was a very robust pace since late last year. Australia’s trade sector continues to fare well, though you would not think so based on our currency. The nominal trade balance is around its record positive high reflecting both strong export volumes (the result of the 2000s mining investment boom) and a high terms-of-trade (prices for our commodity exports are still high by historic standards). Normally, such a positive trade balance would put upwards pressure on the Australian Dollar. It traded around parity with the US$ in the previous terms-of-trade boom in the early 2010s. However, a poor outlook for China’s economy and low interest rates relative to the US are weighing on the A$. The Labour Market Australia’s labour market remains robust at the headline level. The unemployment rate is around a generational low. Employment growth is very strong, running at levels which would normally be characteristic of boom times. However, there are some signs of weakness ahead. Online job applications are beginning to see more applicants, which has traditionally been a sign of higher unemployment. Business surveys also suggest actual hiring and hiring plans have slowed down. Employment tends to lag activity in the broader economy, particularly following a period when it has been very difficult to find employees. As a result, we do not expect a meaningful deterioration until the domestic economy suffers a pull-back. If broad economic weakness is avoided, the labour market will be fine. Source: Drummond Capital Partners, Refinitiv Datastream, Seek Putting it all Together After the most aggressive interest rate tightening cycle since the late 1980s, one could be forgiven for wondering why bigger cracks have not opened up in the Australian economy. Part of the puzzle is population growth, which is currently sitting at around a fifty-year high and is above many comparable developed market economies (see below). In fact, the latest National Accounts showed Australia’s economy per person has shrunk in the past two quarters – effectively a per capita recession. Strong population growth has also had the added benefit (or cost, depending on your ownership status) of putting a floor under domestic house prices, despite household borrowing capacity falling around 30% due to interest rate rises. Another piece of the puzzle is that on average, net household cash flows look OK across the economy. The actual net drag from higher interest rates has not been too bad. Inflation has probably done more damage to aggregate spending. Australia has an economy that looks fine at the nominal level, but once you account for per-person, after inflation outcomes, conditions start to look worse. Another important factor is that the concept of the average Australian household does a pretty bad job of capturing the nuance within the economy. While, in aggregate, households are fine, this masks the substantial deviation in outcomes higher interest rates have generated. Picture two households: (1) a young family who stretched themselves to purchase a home before the RBA started hiking rates (expecting no hikes until 2024), and (2) an older couple with a paid off residence and rental property (benefiting from strong rental price growth) and term deposits now earning a healthy return. At the economy-wide cash-flow level, the wins the older couple are feeling are mostly offsetting the pain of the young family. However, how their spending reacts to the change in circumstances is not going to be the same. The winners often choose to hold back on spending all of their windfall (not expecting it to last) while the reality of budgeting means the losers are forced to cut back spending. We still think the risk to the Australian economy is to the downside. High frequency data, such as our Growth Barometer, suggests the economy is continuing to lose momentum. Higher interest rates will eventually start to drag on the net cash flows of households. Lower household spending will take the wind out of the corporate sector’s sails. This will lead to job losses and people who lose their job cut back spending a lot more than those faced with higher interest rates. Source: Drummond Capital Partners, Refinitiv Datastream Despite the relatively pessimistic economic outlook, our portfolios have a neutral exposure to Australian equities. This reflects a number of things. The outlook for Australia is not really any worse than any other region. All developed markets have too much inflation, rate hikes and slowing growth. Australian equities also tend to be more defensive than global equities in bad markets, and we are in aggregate still worried about the future. Finally, the Australian Government’s fiscal position remains much better than most of the developed world, meaning the capacity for fiscal stimulus on the other side of any recession is large. [1] We have made many assumptions to convert household balance sheets into estimated net cash flows. [2] Financial asset return = 35% ASX200, 35% MSCI World, 30% Australian Bonds. This is prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice. .Australia’s Rate Surprise

Estimated Per Person $ Income Flows[1] (Left) and $ Change in Asset Position[2] (Right)