Market Update – September 2023

19/09/2023Market Update – November 2023

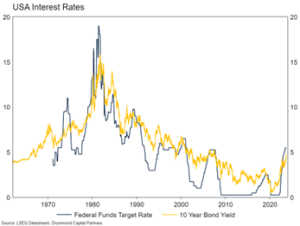

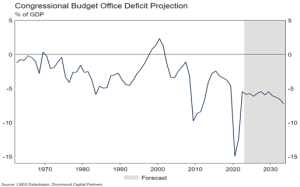

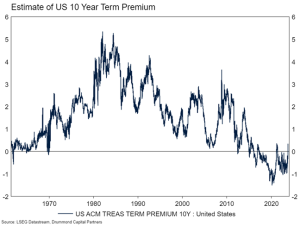

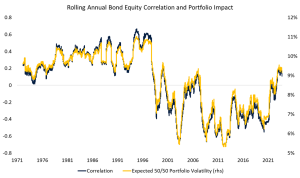

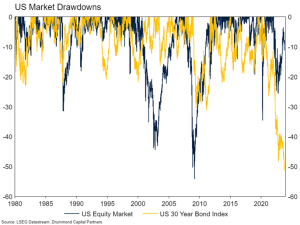

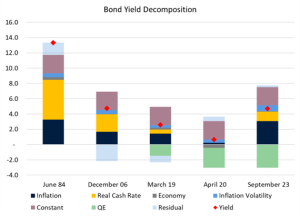

28/11/2023 Key Points: Bonds have been beaten down harder than the Wallabies in the 2023 World Cup. Rising interest rates since mid-2020 have delivered the largest loss in long dated bonds in at least forty years. The loss in US 30-year bonds has now rivalled equity market drawdowns seen in the Tech Bubble blow-up and the Financial Crisis. Shorter dated bonds have also sold off severely. That a defensive asset class has delivered such an outcome will have come as a shock to many investors. In this month’s Market Update, we take another look at bonds. Will the bloodbath continue? Or, as with equities in late 2002 or early 2009, does the historic sell off herald a generational buying opportunity? The key to this question is whether the sell-off is complete, or, if we have simply entered a new (or old, depending on your time horizon) regime of higher interest rates. Why Have Yields Risen? The rise in yields since mid-2020 has been driven by a number of factors. The figure below shows the results of a simple bond model which decomposes the level of the US 10-year yield into broad macro drivers. Much of the fall in yields since the mid-1980s was initially driven by lower real cash rates and inflation, with quantitative easing (QE) having a substantial impact since the Financial Crisis. However, between the 2020 low in bond yields to now, the rise can be in large part explained by rising inflation and real cash rates – a reversal of the previous trend. The impact of QE has moderated from its peak since the Fed began its balance sheet roll-off, but is still material, reflecting the still large stock of bonds on the Fed’s balance sheet. The Bond Outlook By all accounts, developed market bonds looked very attractive to investors from late 2022. There had been substantial capital loss (they were cheap relative to history), inflation had been moderating back towards central bank targets, and many expected a recession on the horizon (which has historically been a good environment to hold bonds, as interest rates tend to be cut). However, after a brief respite, the sell-off has resumed. A good deal of this recent move can be explained by poor bond supply and demand dynamics. The US Federal Reserve is no longer purchasing bonds (quantitative easing), effectively removing a key buyer from the market who has been present for much of the past decade. In addition, the US budget deficit so far this year has been much higher than anyone originally expected. A higher budget deficit means the US Treasury needs to issue more bonds in the market to meet its funding needs, again increasing bond supply relative to demand. Importantly, the outlook for the US budget deficit going forward is bleak, suggesting this supply and demand imbalance will continue. The figure shows the Congressional Budget Office’s projection for the US deficit over the next decade. The increased “risk” of holding bonds due to a deteriorating fiscal situation and high inflation, is reflected in a rise in the estimated term premium, which is effectively the extra return that investors demand to hold bonds versus the expected path of cash rates. The figure below shows one estimate of this premium, which has risen substantially since early 2020, but remains well below historic levels. At least until there is a clear sign that US economic growth is weakening enough that the Fed will be forced to cut interest rates, we think bonds will struggle. US budget dynamics remain poor. The Fed is no longer buying bonds. Progress on inflation in the US has stalled in the last couple of months and surveys suggest most institutional investors are long the asset class, suggesting there is plenty of capacity for further selling. Beyond this, the capacity for bonds to earn back their losses will depend on whether the very low interest rates experienced post the Financial Crisis were an anomaly, and we have reverted to a more normal interest rate regime. We think there is a high chance this is the case driven by the four D’s: Demographics, Deglobalisation, Decarbonisation and Defence spending. Demographics will push real interest rates higher as baby boomers retire and spend their savings in the years ahead. Deglobalisation is a powerful inflationary force. The West is decoupling from China which requires substantial capex spend and creates less efficiency in global trade. Also, government spending associated with the transition to net zero will be a significant inflationary force as is greater spending on military armaments. Higher neutral real interest rates and inflation are a recipe for higher bond yields. In line with this, even if there is a recession and central banks cut short term interest rates, we think prospects for bond yields going back to as low as they were in 2020 are pretty low. Indeed, we could see a scenario where cash rates get cut, but bond yields barely budge, delivering a return to a normal term premium, but not much satisfaction for bond investors. Implications for Portfolios Alongside the negative short term return outlook, the other major portfolio implication from recent bond behaviour is the impact on implied portfolio volatility from the now positive correlation between equities and bonds. The rise in correlation from deeply negative in the 2010s to slightly positive currently has taken the ex-ante volatility of a 50/50 bond/equity portfolio, from around 5.5% to around 9% today – a substantial increase. This has the impact of making the same portfolios look riskier than they did three years ago. Source: Refinitiv Datastream, Drummond Capital Partners Portfolio Positioning The other side of this coin is the increased return which can now be generated from fixed income asset classes. While we are cautious on higher duration (longer dated, fixed coupon) fixed interest in the near term (and therefore, underweight government bonds in our portfolios), high grade floating rate investments (such as, term deposits and Australian investment grade floating credit), are now enjoying attractive yields. As a result, we are overweight these asset classes. This is prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only. The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatement of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance. This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice. .Are Bonds Broken?

Source: LSEG DataStream, Drummond Capital Partners

Source: LSEG DataStream, Drummond Capital Partners