Market Update – March 2020

05/03/2020

Getting Perspective On Markets

16/03/2020

Since our update last week, market action has continued to be exceptional. The icing on the volatility cake was the effective dissolution of OPEC+ on the weekend. After Russia did not commit to production cuts last Friday (which would have supported prices), Saudi Arabia slashed its selling prices in retaliation. This, combined with an already weak oil demand outlook due to Coronavirus, saw prices fall 25%. This oil price collapse and continued virus uncertainty triggered a sharp widening in credit spreads to around 2015 levels. US markets fell 7.6% on 9th March, the 19th largest fall since 1928 and the only daily fall since then greater than 7% outside of the Great Depression, WW2, the Global Financial Crisis and 1987’s Black Monday. For reasons outlined last week, this kind of incredible volatility is likely the new normal. Systematic investment strategies, increased bank regulation and growth in passive investment strategies mean markets are likely to be dysfunctional, mispricing risk both in calm and volatile times.

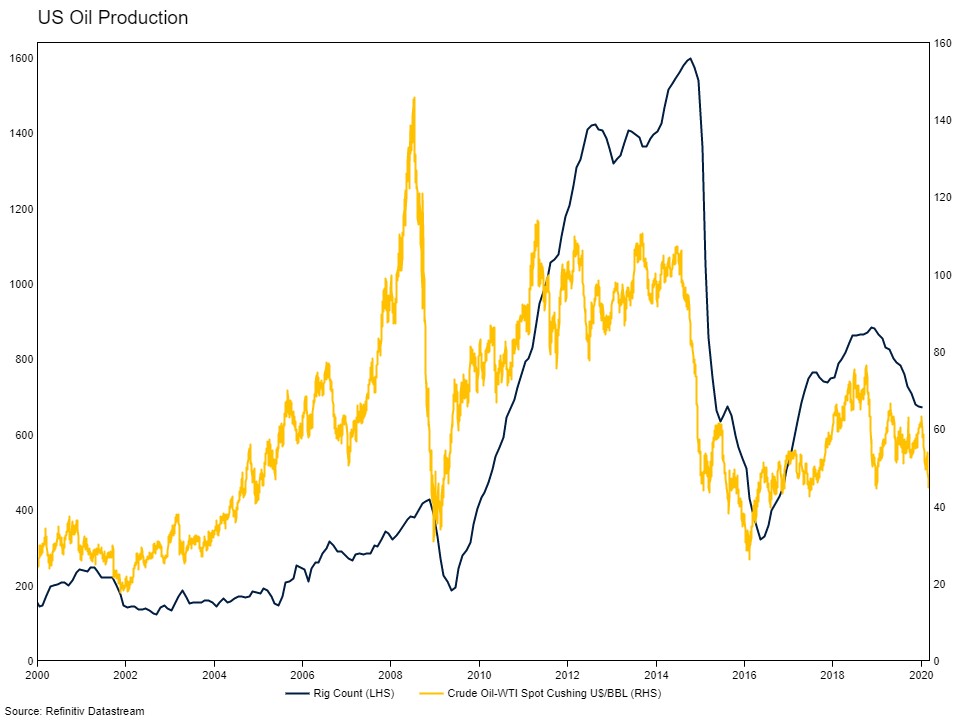

The collapse in oil prices in and of itself isn’t necessarily a material cause for concern. Oil prices have fallen significantly in percentage terms but are only around $30 per barrel lower than in January this year. In the nearly two years from mid-2014, the oil price fell $80 per barrel, from around $107 to $26 per barrel. During the 2014 collapse, the number of shale rigs producing oil in the USA fell from around 1600 to around 300. Currently, there are only 600 rigs in operation given the low starting oil price, though this is likely to fall significantly if oil prices hold where they are. On net, we expect the impact on the US economy from this fall in prices to be less than that faced in 2014 and 2015.

A key consideration is the collapse in oil prices on credit spreads. In 2014, the energy sector accounted for around 15% of both high yield and investment grade bond indexes[1]. While this currently stands at only around 10% in the high yield space[2], the overall credit quality of US corporates has deteriorated since 2015. In particular, there is a huge amount of debt trading just on the cusp of investment grade. It will not take much of a market shock to push these issues back down to junk status, triggering a period of forced selling by institutions which are mandated to hold investment grade credit and passive products. The emergence of listed corporate bond ETFs promising liquidity over an illiquid investment presents an additional challenge to the asset class. The market could gap if investors rush to exit at the same time, which is likely in the event of mass downgrades. This is a risk we have been concerned about for a while and has the potential to turn a short-term external economic shock (Coronavirus) into a systemic risk issue, which would be a catalyst for a much larger drawdown.

Pivoting back to the more clear and present danger to the global economy – the Coronavirus pandemic – the news over the past week has been mixed. On the positive side, it seems as though South Korea has been getting a handle on its outbreak. The number of new daily cases has fallen by nearly a half over the period due to extensive countermeasures. Other countries such as Singapore, Japan and even China have also demonstrated remarkable success in containing outbreaks. We now have available a blueprint to follow in the rest of the world to limit the impact of the virus. Unfortunately, that blueprint comes with a meaningful macro impact. To varying degrees, schools, shops and offices have been closed, freedom of movement has been restricted, personal privacy has been forgone.

It also seems that delayed action requires a larger response. Trying to stem its own outbreak, on Tuesday Italy locked down the entire country, telling people to stay home unless the reason for travel is work, medical reasons or an emergency. To put the speed of required action in context, exactly two weeks ago, Italy had 322 confirmed cases, now there are more than 9000. Put another way, Italy has gone from the same number of per-capita cases as Australia currently has, to locking down the country completely in 14 days.

The problem is that all of this (falling oil prices, credit market dislocations and Coronavirus) is happening at the same time, and as evidenced by recent market moves, creating huge uncertainty and elevated market stress. In times such as these, the sum of risk is greater than the parts. Governments are announcing more stimulus (payroll tax cuts in the USA for example), but we don’t think this will be enough to offset the compounding weakness, at least initially.

While the short-term outlook is still negative, we are quite positive on the medium-term outlook for equities. Once the wave of the Coronavirus passes, and if credit markets do not unleash systemic risks, we will be left with a global economy awash with huge stimulus and consumers that are ready to spend given pent up demand built up during lockdowns.

[1] https://www.bis.org/publ/qtrpdf/r_qt1503f.pdf

[2] https://www.ssga.com/library-content/products/factsheets/etfs/us/factsheet-us-en-jnk.pdf

The information contained in this article is current as at 12/03/2020 and is prepared by Drummond Capital Partners ABN 15 622 660 182, a Corporate Authorised Representative of BK Consulting (Aust) Pty Ltd (AFSL 334906). It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.